109 items found

After a sharp decrease in 2023 with 26% of the take up of logistics real estate in 11 European markets, the take up in 2024 will stabilize. This is one of the conclusions of two studies Buck Consultants International / BCI Global published this morning.

Read more

The EU’s Carbon Border Adjustment Mechanism (CBAM) is a tool to put a fair price to the lifecycle of carbon intensive goods imported into the EU. As per October 2023, CBAM imposes a reporting obligation and carbon tax for companies importing designated goods, full implementation expected on January 1st, 2026.

Read more

In an exclusive report, the expert team at Netherlands-based BCI Global takes a close look at two dozen ‘out-of-the-box’ cities for future software development and support centers.

Read more

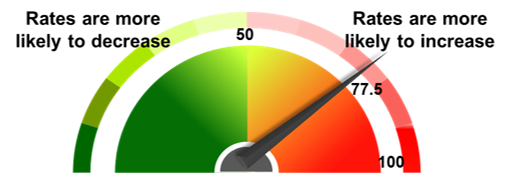

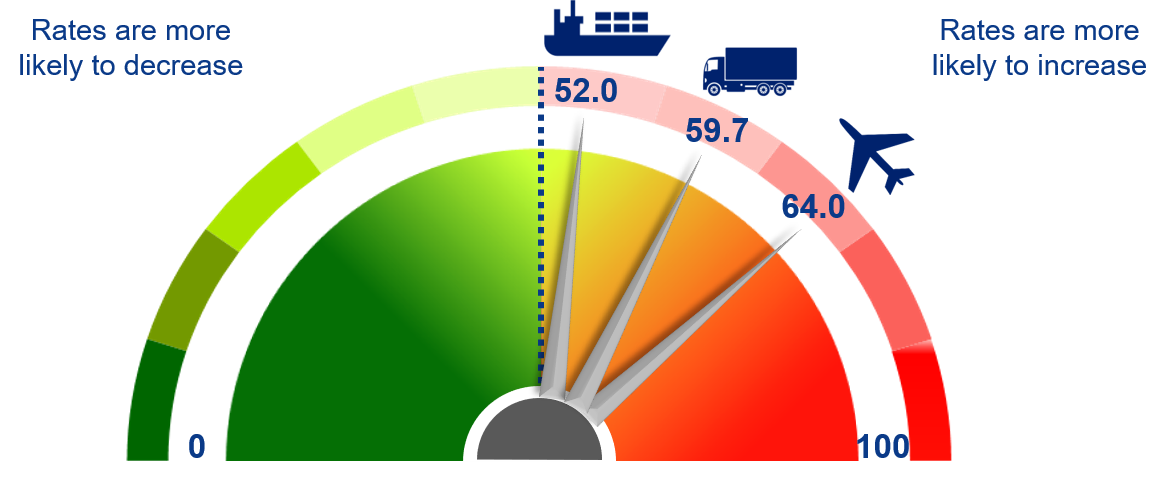

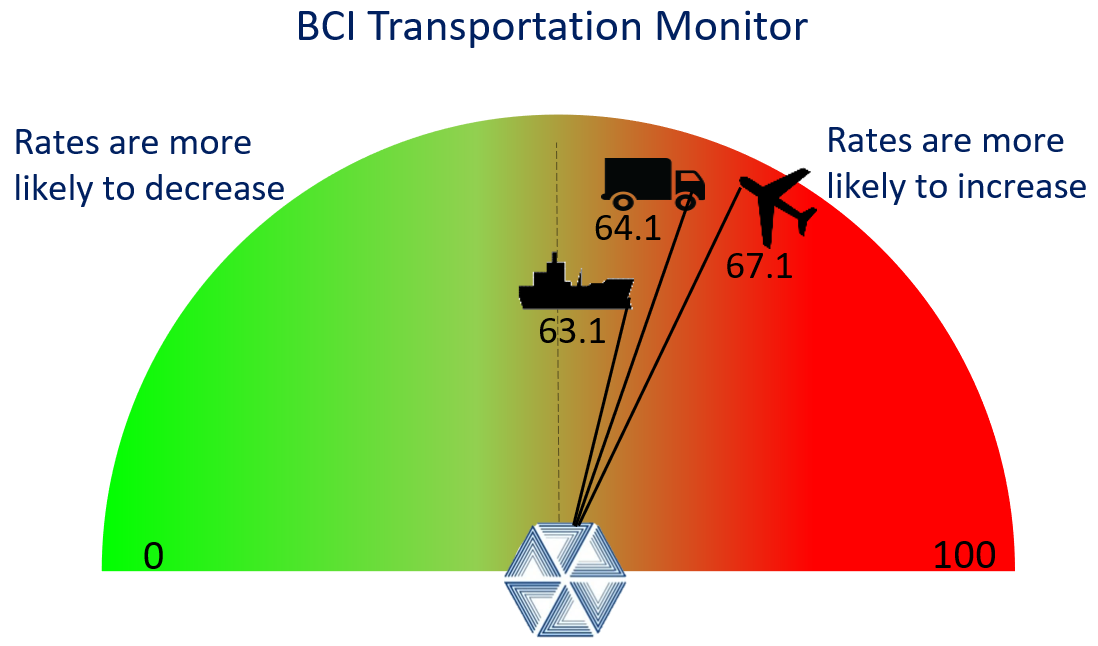

European road and parcel freight rates will increase with 8% in the next six months. Global ocean freight rates are stable at low level, but air freight rates will further decrease with another 5%.

These are one of the main conclusions from the Transport Monitor of leading supply chain and logistics consulting company BCI Global. For the tenth time an esteemed panel of shippers and manufacturers gave their expectations on freight rates developments for the next six months.

Read more

Reshoring accelerates as American and European companies want to de-risk their supply chain from geopolitical developments and supply chain disruptions. This concludes supply chain and location strategy consulting firm BCI Global in a very extensive study (supported by SCM).

Read more

The next years more companies will set-up R&D centers in the major regions of the world (e.g. Europe, North America, Asia).

This expectation was presented at the World Conference of the International Association of Science Parks (IASP) in Luxembourg by René Buck, CEO BCI Global.

Read moreThe renowned international business magazine Forbes Magazine has announced that the economic, logistics, and real estate advisory firm Buck Consultants International/BCI Global is among the best management consulting firms in the world.

Read more

One of the most influential financial and economic platforms in the world Bloomberg paid attention today to our new DE-5 Proprietary Framework for Value Chain Management.

The framework aims to reduce risk in five major areas linked to the operations of many multinational companies. While there are vast differences between various companies and industries, these five points guide companies in working to ensure sustainable and resilient operations.

Read more

The Netherlands is a major logistics gateway to the ever growing European market of more than 500 million customers. But where do you start in finding the right Dutch logistics service provider for your European distribution operations?

BCI Global offers you the annual overview of the top-100 Logistics Service providers in the Netherlands as a comprehensive tool for selecting the right logistics company for your European logistics business.

Read more

More than 250 new plants of battery producers and their suppliers will be established in Europe in the next 10 years.

That concludes international consulting firm Buck Consultants International in an analysis of the future European batteries market, presented today at the Transport Logistic exhibition in Munich.

Read moreBCI Global among America's Most Admired Companies to Watch

California based CIO Bulletin, the leading platform for Business & Information Technology leaders, has recognized BCI Global in its latest issue as one of Americas 50 Admired Companies to Watch 2023.

Read more

Greening end-to-end supply chains is possible without jeopardizing competitive cost levels and customer service requirements

Integrating carbon footprint reductions is in many supply chains a realistic objective, without a huge cost increase or lowering the customer service level. An end-to-end approach to ‘green’ inbound transportation, the warehouse itself and outbound transportation is mandatory to get the best results.

Read more

Thou shalt… test and reimagine supply chain scenarios

In recent decades, supply chains have become longer and more complex due to globalization. Access to global markets and the ability to manufacture in low-wage countries with low or no import taxes have produced supply chains that are very efficient, but not resilient. This lack of resilience has become abundantly clear in the past two years, due to the pandemic, the war in Ukraine, the energy crisis, the global geopolitical situation and the high number of production and logistics-related disruptions in supply chains.

Read more

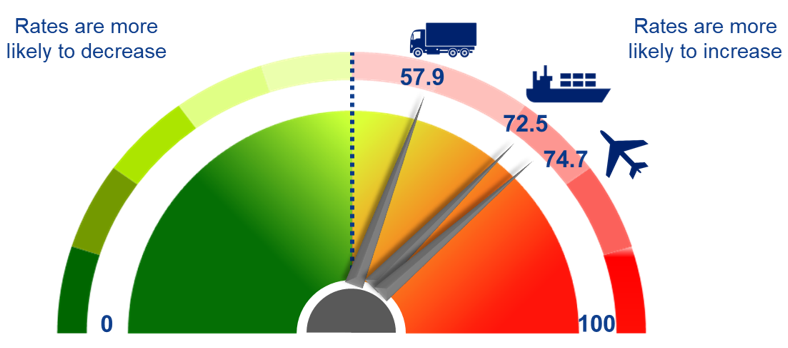

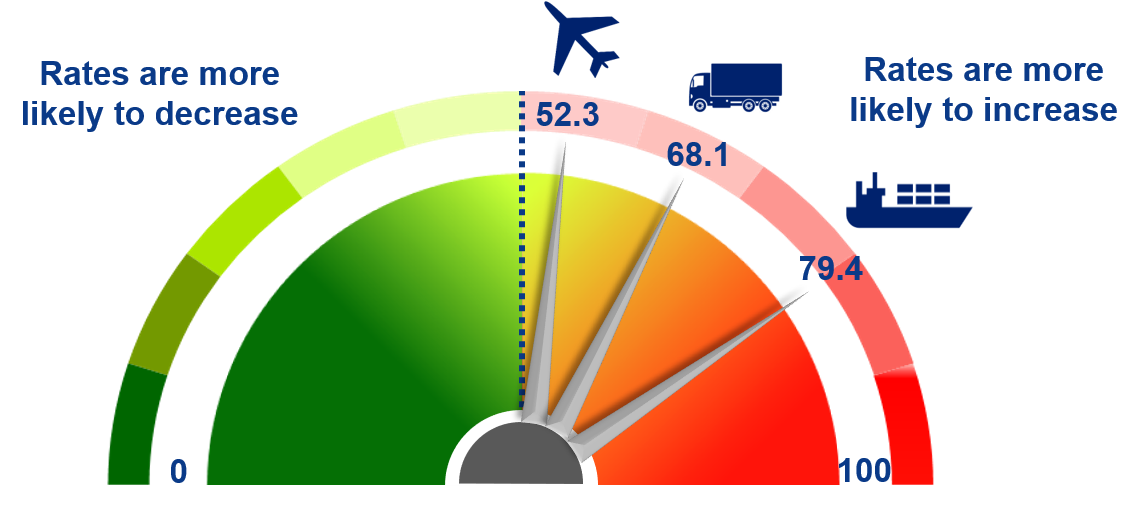

European road transport rates for parcels & pallets continue to increase with 5 to 10+%. Ocean rates are still going south, while Airfreight rates remain extremely volatile. Cargo owners shall maintain different procurement strategies for securing competitive pricing.

In addition the European Commission adopted new Corporate Sustainability Reporting Directives (CSRD), meaning that Cargo Owners need to report and reduce Carbon Emission of Scope 3 activities that include (outsourced) transportation and logistics.

Read more

Supply Chain challenges caused by demand volatility, labor scarcity and quality of 3PL performance were discussed including various measures to deal with these, at our roundtable in Fashion and Luxury industry.

On Wednesday September 5th we organized and moderated a round table for VP’s in the Fashion and Luxury e-commerce industry. Michael Kors hospitably invited us at their European DC in Venlo and provided a tour in their location for this event.

Read more

Global air and ocean transport has been causing major headaches to supply chain leaders but European road transport remained rather stable. Road transport rates are expected to rise by 5-8%. Five tactics to mitigate the current impact on European road transport will be detailed.

Read more

The Netherlands is a major logistics gateway to the European market of more than 500 million customers,even in these unprecedented times. Many American and Asian shippers are using the Port of Rotterdam and/or Schiphol Airport to supply European customers, and have set up European Distribution Centers in the Netherlands. A wide array of logistics service providers in the country are offering a various activities and operations to international shippers, ranging from simple transport, handling and storage to tailor-made value added operations. For all major supply chain operations, a best-fitting logistics service provider can be found in the Netherlands. But where do you start in finding the right Dutch logistics service provider for your European distribution operations? BCI Global can offer you an comprehensive overview of the top-100 Logistics Service providers in the Netherlands.

Read more

Never before have the vulnerabilities of complex global supply chains been so exposed as today. Long and unreliable lead times, lack of capacity across the supply chain, congestion at ports, suppliers unable to deliver to promise and number of customer orders going through the roof. If a company is not able to create the necessary visibility and control in its supply chain this will seriously jeopardize the business. To support brand owners BCI has developed a framework with 6 tactics to create control in these uncertain times.

Read more

Over 60% of European and US companies expect to reshore some of their production activities from Asia back to Europe or the US over the next three years. In most of these cases it is about limited volumes and/or critical parts and products, but 17% intend to bring back the majority of their Chinese and Asian production capacity. When it comes to Europe, Central and Eastern Europe is in favour for new production locations, especially countries like the Czech Republic, Poland and Hungary. Germany and Benelux countries are also being considered as serious options (by 48% and 38%, respectively). When reshoring production to North America, the US itself is the preferred location, followed by Mexico.

Read more

Legal firms are looking at ways to optimize their legal services as the conventional way of working 100% in the office has been radically challenged during the pandemic. Now, many legal firms expect growth across most global geographies and are re-evaluating their location strategies. Right-shoring turns out to be different for different players

Read more

As customers worldwide combine online buying with physical shopping, companies have to organize their supply chain in a seamless way, offering the consumers one great experience. But how to do that and what are the IT platform requirements?

Read more

The shortage of software developers is pushing companies in Europe to become more creative regarding sourcing new talent and developing future proof location strategies. In order to assure the required software talent in Europe, an in-depth assessment of candidate locations is the key to success: at the end of the day there is no lack of talent if you are the preferred employer.

Read more

Over 60 percent of European and US manufacturing companies expect to onshore or re-shore part of their Asia production in the next three years. In the majority of these cases it is about limited volumes (minority of the volume) and/or critical parts and prod-ucts. But one out of five companies expects to repatriate even the majority of the China and Asia production capacity

Read more

Online shopping is booming for digital native and brick&mortar companies alike. Selling online direct-to-consumers (D2C) is more and more important. But selling D2C requires a more advanced supply chain and a more mature logistic service provider.

Read more

The European logistics market has grown last year with a record number of 10% and a further growth of the take-up to nearly 34 mln sqm is expected for this year. The logis-tics markets in the UK, Germany and France are still hot, not only from a tenants per-spective (high take-up), but also from an investor perspective as yield compression continues and yields are expected to decrease with 40 basis points.

Read more

The general rate increase (GRI) for parcel and express shipments in Europe will this year be between 4% and 7% (4-6% domestic; 5-7 cross border). That is one of the results of the 6th edition of the Transport Monitor of BCI Global.

Read more

Biopharmaceuticals are one of the world’s growth powerhouses. In 2020, the global biopharmaceuticals market was worth $325 billion, and it is expected to grow with a compound annual growth rate of between seven and eight percent to approximately $500 billion in 2026, according to Mordor Intelligence. This growth is being driven by the aging of populations in major markets, increases in chronic diseases and the development and acceptance of new innovative therapies in areas such as cell and gene therapy and precision medicine.

Read more

Although the vast majority of multinational companies already has some sort of support model in place, the global Support Services market is still expected to mature and grow further with 4 billion USD until 2027. Companies are now focusing on process efficiency, added value, digitalization and innovation. Also, many companies are using their best service delivery models to also target emerging markets. What key trends are taking place in the Support Center market and what does this mean for the global right-shoring location strategies for Support Centers?

Read more

The US economy is ‘hot’. Fueled by the Covid-19 recovery with a forecasted economic growth of more than 5 per cent this year and the substantial investment packages of President Biden domestic and foreign companies are investing in new manufacturing plants. But labor market challenges are around the corner.

Read more

For most companies clearly the time has come to take a longer-term perspective again and prepare the company for potential new disruptions in the future. BCI Global has defined 5 strategic initiatives that companies should adopt when preparing the manufacturing footprint for the future.

Read more

E-commerce has grown 2-5 times faster than in the pre-pandemic period in literally every country and double digit annual E-commerce growth is reported by almost all businesses. It will not be a surprise that this will continue the next coming years. According to CBRE research the E-commerce global sales by 2025 will amount up to a staggering number of $3.9 Trillion USD, as opposed to $2.4 Trillion USD today.

Read more

An integrated approach focusing on Visibility, Affordability, Resilience and Sustainability helps to cope with the current transport challenges. BCI Global has developed this so-called VARS framework to support companies improving their transport operations.

Read more

Distribution centres are becoming more and more relevant for spatial planning, due to their rapidly increasing size and number. There is little literature, however, that provides a generalized analysis of the size and functional attributes of distribution centres, and none that discusses the relationships between these attributes.

Read more

Currently, there is a serious storm or even a hurricane ongoing in the ocean freight industry. Rates are at an all-time high (BCI’s monitor shows an average of factor 4, with outliers of factor 10!), capacity is limited which is strengthened by the false container positioning and port congestion due to Covid-measures and high demand is counted in weeks instead of days. The reliability of ocean freight is all time low which pushes the need for end to end visibility even further.

Read more

There is a lot of uncertainty about what the post-pandemic future of work will look like, there are quite opposing views with strong voices for “Keep working from home” versus also a plead for “Let’s go back to the office”. How are you going to make the strategic choices? Are they different for the various types of office operations you have? Which key factors have to be included in your considerations? Is more or less office space needed? And as a result; will your footprint and location strategy change?

Read more

The Netherlands is a major gateway to the European market, even in these unprecedented times. Many American and Asian shippers are using the Port of Rotterdam and/or Schiphol Airport to supply European customers, and have set up European Distribution Centers in the Netherlands. Many logistics service providers in the country are offering a wide array of activities/ operations to international shippers, ranging from simple transport, handling and storage to tailor-made value added operations.

Read more

SHINE Medical Technologies LLC has announced that it has selected the municipality of Veendam in the province of Groningen, the Netherlands, as the location of its European medical isotope production facility. The decision is the culmination of a year-long search process that included the review of more than 50 proposals from sites across Europe. BCI Global supported Shine Medical in its location decision process.

Read more,-frankfurt,-germany.jpg)

European logistics real estate markets have not suffered last year from the Covid-19 pandemic. Due to fast growing e-commerce and higher inventory levels of producers the total expected take-up in 11 European countries of 23.6 mln sqm for 2020 is only 3% down compared with record year 2019. In major markets like Germany and the UK last year’s figures were certainly not bad.

Read more

In the last five years, the number of operational rail services on the New Silk Rail Route between China and Europe has grown to about 150 rail shuttles per week. These rail container shuttles connect over 30 European cities with 16 regions in China. Are these regular rail services between China and Europe here to stay in the coming years? What is the impact on the services of the COVID-19 pandemic? And are there any new site location trends in Europe?

Read more

The new Silk Rail Routes between China and Europe have shown a fast growth with an increase of 50% in volume and 100% in value in the last five years. Currently, about 150 trains per week run between 30 European location and 16 regions in China.

Read more

All over Europe the growth can be seen of mega distribution centers (> 40,000 sqm) of manufacturers, (r)etailers and logistics services providers. XXL warehouses increase efficiency and are also able to offer the space for the fulfilment of on-line sales as more stock has to be held and ample room for handling of returns is necessary.

Read more

In the period 2013-20191) 424 Mega Distribution Centers (each more than 40,000 sqm floor space) have been established or announced in the logistics heart of Europe. The majority of them were built in Germany (285; 67%), followed by the Netherlands (98; 23%) and Belgium (41; 10%). Altogether these 424 XXL warehouses have 28.9 mln sqm floorspace.

Read more

Often shippers are dissatisfied with the relationship and the service they get from their Logistics Service Provider (LSP). Recent research learns that more than 50% of shippers consider changing LSP or to insource part of outsourced operations. The reasons for the dissatisfaction vary greatly: non-compliance with contractual Key Performance Indicators; insufficient knowledge of the specific market and industry; not flexible enough; lack of IT capabilities; too little attention for new technologies; too high rates; and insufficient drive to proactively continuously improve on performance and cost levels.

Read more

Attractive incentives and tax deductions have always the interest of companies considering to set up new operations wherever in the world as financial packages can reduce investment and annual operating cost. But Covid-19 causes hurdles, but also new opportunities

Read more

Managing freight costs is key for supply chain and logistics professionals. The Covid-19 crisis makes companies even more aware that creating visibility and optionality in transport and logistics is a must. The BCI Transportation Monitor will assist you how to manage costs and provides five strategies how to create optionality and visibility in transport and logistics during Covid19 crisis and beyond.

Read more

BCI Global has made it for the second year in a row to the Forbes 2020 list of America’s Best Management Consulting Firms. The prestigious business magazine Forbes released in March this year its annual listing of best management consulting firms. The economic, location and supply chain consulting firm BCI Global (Buck Consultants International) is one of the selected firms.

Read more

Covid-19 made the dependency on manufacturing and sourcing in China visible, leading to vulnerable, interrupted supply chains. Combined with increasing production costs (particularly in China’s East Coast provinces) and the trade and geopolitical tensions between the US and China (and to be expected between Europe and China) Western companies are looking for alternative production locations in South East Asia.

Read more

Due to covid-19 driven lockdowns and social distancing measures, an unprecedented work-from-home strategy is impacting all office-related operations around the world. You can read quotes of CEO’s saying their employees can now forever work from home, but on the other hand a lot of employers fear less creativity and lower productivity levels of teams when they only meet online. What is your new strategy?

Read more

Covid-19 has exposed the vulnerabilities of global complex supply chains. Many companies are faced with a lack of end-to-end visibility. Do you stay in the dark or develop a control tower?

Read more

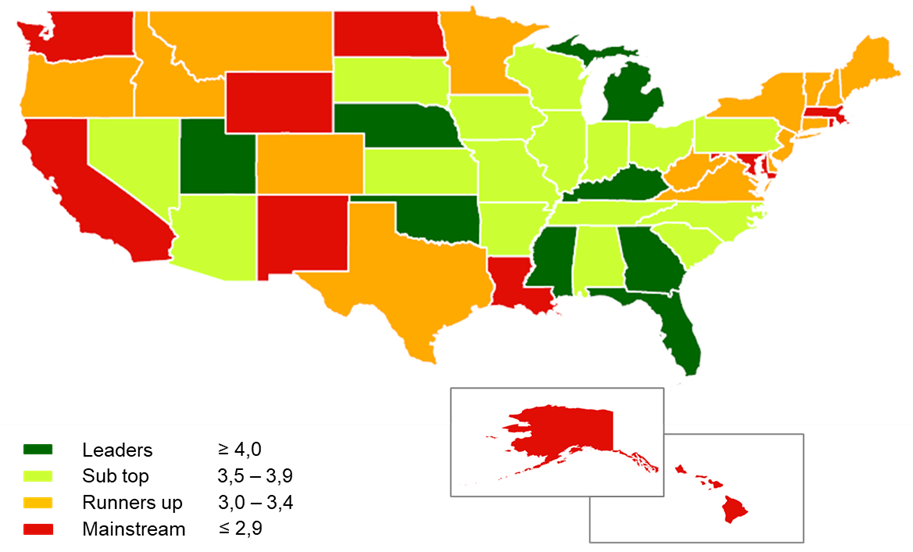

BCI Global’s new US States Manufacturing Competitiveness Index, shows a ranking for Industrial Manufacturing Competitiveness based on comprehensive cost, quality of the business environment and risk analyses for an illustrative case. Here are the top 24 States, with 8 leading States and 16 in the sub-top.

Read more

Decentralization of production, also known as re-shoring from China/Asia back to North America or Europe, is at the top of the agenda in many corporate boardrooms. What are the advantages and disadvantages of various manufacturing strategies and how does a real life reshoring business case look like?

Read more

Oxea, a leading global manufacturer of oxo intermediates and oxo derivatives, has decided to build a new acid plant in Oberhausen, Germany. BCI Global was part of the team assessing several location scenarios and developing the business case.

Read more

As the traditional supply chain risk approaches fail, the key question is how to incorporate risk resilience in your supply chain. BCI has developed a Resilience Framework to assess risks and to make explicit trade-offs in terms of risk management, resilience and investments.

Read more

China’s size, economic growth (despite Covid-19) and fast development of internet sales are unique in the world. More and more people buy online: today 35% in China is e-commerce sales, expected to increase to ~65% over the next 3 years. This means that the e-com channel strongly develops and this requires another product to market approach.

Read more

Covid-19 has demonstrated the benefits of having stocks and surplus capacity available. Safety stocks and unused capacity in Lean Manufacturing are seen as waste, rather than a cost of doing business. Have supply chain professionals been overshooting in “leanification”?

Read more

The Netherlands is a major gateway to the European market, even in these unprecedented times. For all major supply chain operations, a best-fitting logistics service provider can be found in the Netherlands. But where do you start in finding the right Dutch logistics service provider for your European distribution operations?

Read more

The European logistics real estate markets suffer from the impacts of Covid-19. In 9 important logistics real estate markets the take up in 2020 will be 32% less compared with 2019 if business returns to ‘normal’ as of October 1st. If the business circumstances are back to normal only as of January 1st, 2021 the total new take up will decrease with 46% compared with last year.

Read more

The majority of Chinese manufacturers, retailers, e-tailers and logistics service providers are succeeding in getting back on track now that the country has passed the peak of the coronavirus outbreak. Two-thirds of them are already at 80% or more of their capacity. Nearly 60% of manufacturing companies mention that their upstream supply chain (i.e. supply of components and sub-assemblies) has basically returned to normal, and the same applies to 47% of logistics services providers.

Read more

Two-thirds of Chinese manufacturers, (r)etailers and logistics services providers are already on 80% or more of their capacity. Nearly 60% of the manufacturing companies mention that their upstream supply chain (i.e. supply of components, sub-assemblies) has basically returned to normal; the same applies to 47% of logistics services providers.

Read more

Pressure from governments and other parties that provide funding to achieve economies of scale push International Non-Governmental Organizations (INGOs) to new organizational models as cost effective INGOs have better access to funding. Various organizational models and location strategies are possible, what is the most optimal set-up?

Read more

Effective external risk management is a complex task involving a combination of operational strategy and mitigation techniques. Rene Buck, CEO of Netherlands based management consultancy, BCI Global, tells us more about business disruption risks and methods of coping with them.

Read more

The transportation costs represent 50% or more of the supply chain spending, because for many companies transportation of goods is the highest operational supply chain expense. Therefore, managing freight costs is key for Supply Chain and Logistics professionals. The BCI Transportation Monitor will assist you to define you freight procurement strategy and tactics.

Read more

The Netherlands is one of the major gateways to the European market. Many logistics service providers are offering a wide array of activities and operations to international shippers, ranging from simple transport, handling and storage to tailor-made value added operations. For every specific European supply chain, a best-fitting logistics service provider can be found in the Netherlands. But where do you start in finding the right Dutch logistics service provider for your European distribution operations?

Read more

For more than 10 years now software developers have been amongst the top-3 hardest to fill jobs all over the world. Selecting the right location in order to attract, (re)train and retain software developers and building a pipeline for tomorrow is a key to success.

Read more

Business Worldwide states the following in a press release. The founder and CEO of BCI Global has been named “Best CEO in the Management Consulting Industry” in the 2019 Business Worldwide Magazine CEO Awards.

Read more

India is known for its highly complex tax regime in the past. Under the country’s reform spearheaded by Mr. Modi, the current prime minister of India since 2014, India has revolutionized their complex tax structure with the introduction of Goods & Service Tax (GST). This change is highly welcomed by foreign investors. In last 5 years, there are new foreign direct investments into India. The biggest changes are seen in business and their supply chain models.

Read more

Data is everywhere and data analytics is hot. Especially supply chain network design requires a good portion of data to carry out fact-based decision making. Data collection and baseline development are often cumbersome process steps due to a lack of structure and data gaps. There are 5 key tips to keep focus on what is important, and making baseline development an easier and less time consuming task.

Read more

Many companies seek to start S&OP by selecting a software tool. However if a company is yet to start an integral process like S&OP, it needs to tear down the walls between teams and functions and stimulate cross functional cooperation. This is often underestimated in making a successful change for S&OP.

Read more

Greater agility enables companies to meet demands of flexible and mobile consumers. Speed enhances companies’ growth by responding to shifting market trends. How should Fashion and Lifestyle companies structure their supply chain to create the required responsiveness and speed?

Read more

Global trends and technologies that emerge and develop with an enormous pace impact the Supply Chain heavily. Technologies as blockchain, Artificial Intelligence (AI) and Internet of Things (IoT) are on the rise, fueled with an increasingly complex and dynamic business environment (e.g. US-China trade war, the Amazon effect).

Read more

New analysis of Buck Consultants International on The Future of Logistics Real Estate in Europe released at the Expo Real Conference and Exhibition in Munich, Germany.

Read more

US based SupplyChainBrain is the world’s most comprehensive supply chain management information resource. Bob Bowman, Editor in Chief of SupplyChainBrain interviewed René Buck, CEO of BCI Global on “The US-China Relationship: trade or tech war?” in Los Angeles.

Read more

Finding the optimal location for new Support & Services Centers has always been talent driven. But now technical skills are becoming decisive and this has a profound impact on location decision processes.

Read more

For many companies transportation of goods is the highest operational supply chain expense. It is not uncommon that transportation costs represent 50% or more of the supply chain spending. Despite transportation rates being volatile, the all-time low prices over the last years will not be the standard for the future.

Read more

Technologies as blockchain, Artificial Intelligence (AI) and Internet of Things (IoT) are on the rise, fueled with an increasingly complex business environment (e.g. Brexit, the Amazon effect, US-China trade war). This forces companies to rethink their Supply Chain towards a more repetitive and proactive attitude.

Read more

Many Life Sciences companies are not benefiting from innovative supply chains and technologies. Managing and rationalizing the supply chain from a cost and quality perspective is not a key priority for business executives. For high margin products the focus is often on de-risking the supply chain.

Read more

Nijmegen, the Netherlands headquartered consulting firm BCI Global has made it to Forbes’ 2019 list of America’s Best Management Consulting Firms. Yesterday, the prestigious business magazine Forbes released its annual listing of best management consulting firms. The economic, location and supply chain consulting firm BCI Global (Buck Consultants International) is one of the selected firms.

Read more

Fuel cells create opportunities for safe, reliable, and sustainable energy production. There are four drivers behind the current increasing interest on fuel cells: declining supply of lithium-ion batteries; increasing worldwide government support; phasing out of battery-powered electric vehicles incentives; and upcoming high private investments.

Read more

Results from a Buck Consultants International analysis of the future attractiveness of the United Kingdom in the case that next week’s discussions in the British Parliament result in a no deal hard Brexit.

Read more

Imagine a company that has a fantastic new drug or medical device in the pipeline. Successful market launch around the world becomes life critical for this company. Based on our experience BCI Global has defined four building blocks that help companies in these situations to “guarantee” a flying start.

Read more

Intensifying trade disputes (US-China, US-Europe), the Brexit, reduced economic growth expectations, but also new production technologies demand a review of your company’s global/regional manufacturing footprint. BCI Global presents 4 takeaways.

Read more

Many multinational companies have already put in place various kinds of control towers – initially focusing on creating transactional visibility throughout the supply chain. The physical world of control towers is now meeting the world of planning in so called end-to-end control towers.

Read more

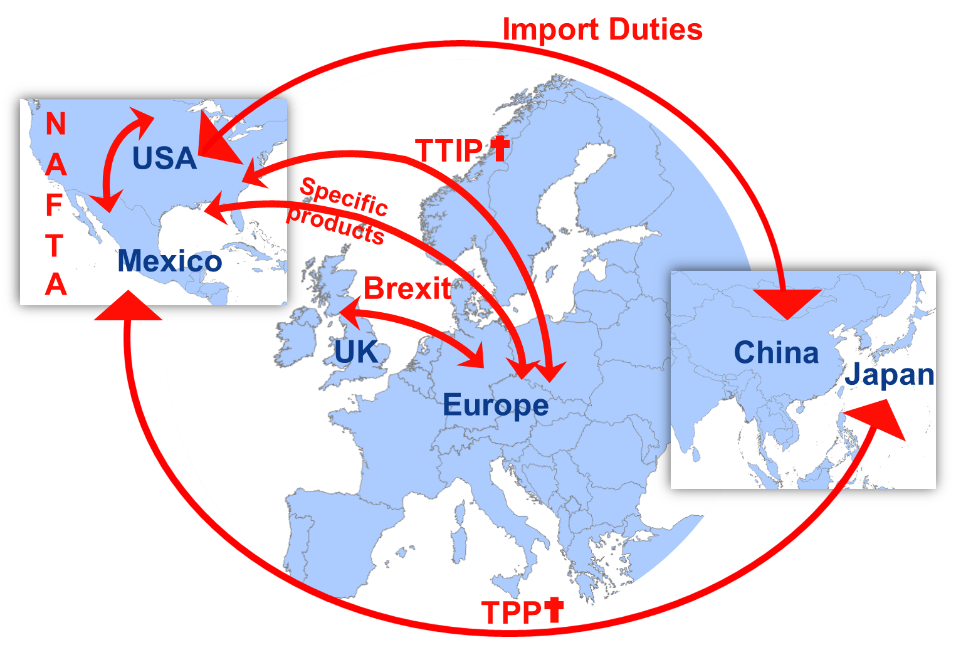

Trade disputes between US, China and Europe are very probably not over soon. BCI has identified and developed 12 strategies how companies can cope with importing and exporting trade tariffs around the world.

Read more

Availability of the right people, increasing labor costs and the need for changing skills set are key issues for many companies. Finding optimal locations for new (production, distribution, service) operations in the US, Europe and Asia is becoming more and more talent driven. But how to identify locations which are future proof from a labor market perspective?

Read more

Robots in warehouses are already a reality and from a technical point of view it would be logical to assume that robots will be implemented on a large scale. But are robots also the right solution from a strategic business point of view?

Read more

Global biopharma and medical devices companies operating in Asia have chosen the Netherlands headquartered consulting firm Buck Consultants International as best Supply Chain Consulting Partner.

Read more

In order to win the R&D rat race companies adopt three supplementary strategies: higher R&D expenditures, open innovation (intensive co-operation with universities, technological institutes, start-ups) and gobalisation, driven by.......

Read more

Strikes at the port of Long Beach, labour disputes in France, natural disasters like an earthquake in Indonesia, a volcano eruption in Iceland grounding air flights between Europe and the US: they all disrupt supply chains.

Read more

Detroit based Gentherm, the global market leader and developer of innovative thermal management technologies, has opened a new production site in Prilep, Macedonia. Buck Consultants International assisted Gentherm’s European management with the site selection process.

Read more

Many brand owners and retailers still have a P&L for each distribution channel: one P&L for their retail channel, one for e-commerce and one for the wholesale channel. Logistics is also organized per channel (‘silo’). But if you put the customer in the center, you need an omni channel strategy to accommodate buy everywhere – shop from everywhere - return to everywhere.

Read more

Economic development agencies all over the world often present themselves in the same way: brochures, interactive websites, regular e-mail updates about always crucial new investments, flash drives with – if printed – hundreds of pages of background information. But who really reads this?

Read more

Customers all over the world expect the same for spare parts deliveries: same or next day delivery, products always available, choices for delivery points. And in the US and Europe that is not a problem. But how to deliver spare parts and meet these expectations in Saudi Arabia, Kenya, Nigeria, Iran, South Africa?

Read more

Big, bigger, biggest. It looks like a rat race but economies of scale urge shippers and logistics service providers to establish mega distribution centers (more than 400,000 sq feet or 40,000 sqm).

Read more

Illinois based agricultural equipment manufacturer GSI opened a year ago its first European manufacturing plant. Location of choice is Biatorbágy (Hungary), where 125 people now work in a brand new facility.

Read more

Supply chain strategies determine the number, size, activities and location profile of distribution centres as 80 per cent of the value chain’s life-cycle costs are locked in at the start with the footprint of distribution centres (and production plants). The direct relationship between supply chain strategy and location choices also means that location choices have a direct impact on the three drivers of shareholder value: growing revenues (due to geographic expansion), costs and capital deployment. The author presents a proven location decision tool (the cost-quality-risk model), in which all relevant cost factors, quality of the business environment factors and risk factors are included.

Read more

Pfizer, AstraZeneca, Novartis, Merck proof it these days once again: the pharmaceutical business is one of the most globalized industries in which new successful medicines are priority number one. But creating responsive supply chain models has become a priority as well. Why?

Read more

Do you recognize one or more of the following questions: Does our supply chain provides the right service to our customer? What is the performance of our supply chain? How to reduce cost in the supply chain? The new BCI Supply Chain Assessment Tool (SCAT) can give you the answers.

Read moreDubai based Emirates Airlines has announced it will open its seconds customer contact centre in Europe with a 300 seat facility in Budapest this year. Europe is a strategically important market for Emirates and this new facility in Budapest will play a critical role in supporting the airline’s growth plans across the continent.

Read more

Hogan Lovells, a leading global law firm, is to set up a Legal Services Center in Birmingham, United Kingdom to deliver high quality cost-effective legal services for aspects of its client work. The Center will operate as an extension of the firm's London office.

Read more

The report is the result of an industry wide research and interviews with leading companies such as Levi’s, Foot Locker, Adidas, Polo Ralph Lauren, Urban Outfitters and VF. The study identifies and discusses eight key developments from a supply chain management perspective, from within the European fashion and lifestyle sector.

Read more

Forget the old score cards and welcome real time information about where products in the supply chain are actually right now. Real time information makes anticipation on global supply chain risks such as natural disasters or sudden delivery problems of suppliers possible. The message: more visibility made possible by smart control towers.

Read more

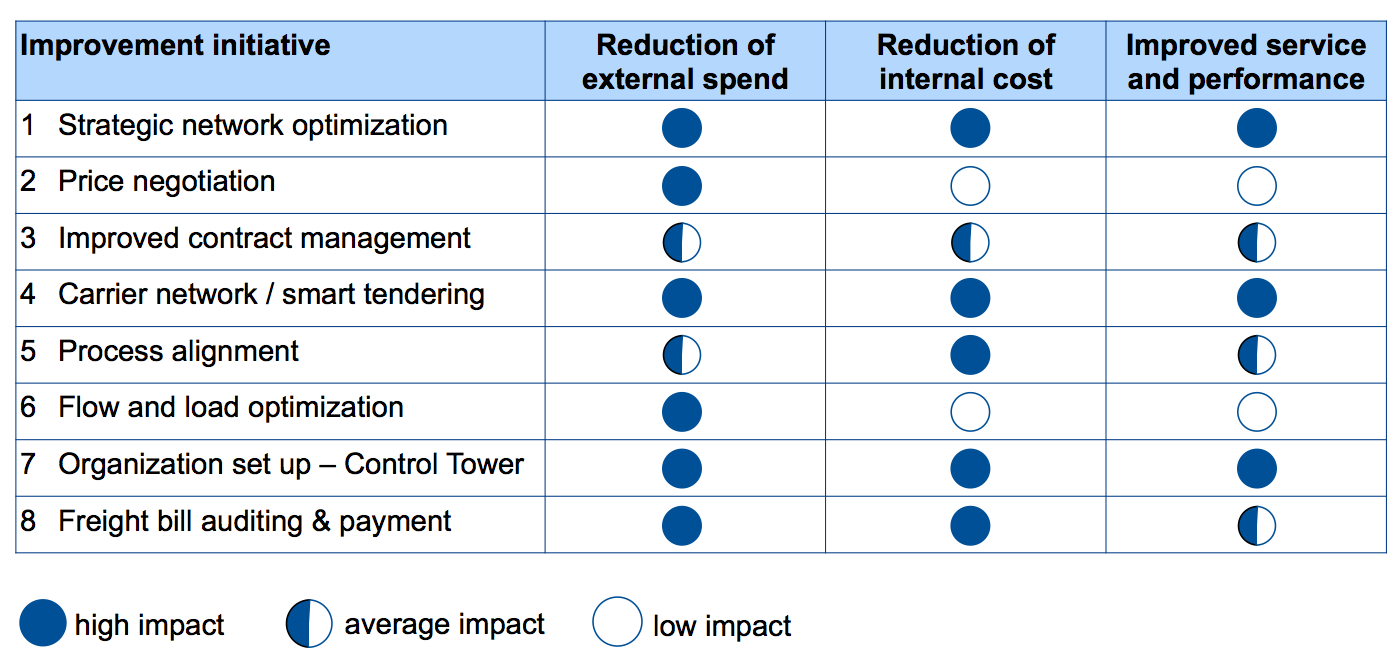

Every supply chain or transportation manager has 4 key objectives: lowering transportation cost, improving service to (internal) customers, improving visibility and improving (financial) control. Buck Consultants International has identified 8 transport improvement initiatives, which address these objectives.

Read more

Rule 1 Position your port/region in new logistics networks Different industry sectors prefer different supply chain set-ups. While computer, spare parts and microchips are often supplied from a central European distribution center, other sectors like pharma and medtech choose more regional distribution centers. And fast moving consumer goods, food and clothing have typically a two tier supply model, with regional distribution centers and satellite DCs. It is important to find out in which supply chains your port, city or region fits best.

Read more.jpg)

The good times with more or less guaranteed high margins are over for pharmaceutical companies. The coming years, reduced costs, greater agility and improved speed to market - whilst ensuring the often complex regulatory legal framework in countries are being met - will form a challenging operating landscape for companies in the industry. Buck Consultants International drafted a white paper which outlines a strategic agenda companies within the industry have to review. "Key to this agenda is the changing commercial business model pharmaceutical companies are starting to address. Pharmaceutical companies will have to turn more towards direct sales channels and therefore also direct distribution models to reduce margins in their current business. This includes direct deliveries to the patient", says Eelco Dijkstra, senior consultant Buck Consultants International.

Read more

The new Janssen European distribution center centralizes the activities of 15 logistics centers in Europe. It reduces the number of steps in the supply chain, with medicines going directly from the manufacturing plants – Beerse (Belgium), Latina (Italy) and Schaffhausen (Switzerland) – to the La Louvière distribution center, from which they are shipped to Janssen operating companies in 11 European countries as well as to Johnson & Johnson affiliates in the rest of the world. Once fully operational the new distribution center will also ship Janssen pharmaceutical products directly to wholesalers, pharmacies and hospitals in Europe. The La Louvière logistics center has a total operational surface of 21,500m² and will handle 160 million packs of medicines a year. Buck Consultants assisted Johnson & Johnson with the international location search for this state-of-the-art distribution center.

Read more

Law firm Allen & Overy is active in 26 countries with more than 5,000 employees. Wim Dejonghe, A&O’s managing partner of the London based so called ‘Magic Circle’-company, indicates that Belfast is not chosen because of the low cost.

Read more